The Economics of the MSO: Where the Money Lives, and Why It Matters When You Sell

If you've read our earlier post on the seven steps to transforming your law firm into an MSO structure, you understand the architecture: two entities, a clean line between legal and non-legal functions, connected by a Shared Services Agreement. What that post doesn't fully answer is the question most firm owners eventually get to: where does the money actually go, and how does this structure make me wealthier than I would be if I just kept running my firm the way I always have?

That's what this post is about.

Two Companies, Two P&Ls

The first thing to internalize about the MSO model is that you're not reorganizing your firm — you're splitting it into two separate businesses with two separate income statements. Understanding which functions belong where is the foundation of everything.

What stays in the law firm (the PC): Attorneys, paralegals, case strategy, client relationships, fee agreements, settlement authority, trust accounts, and bar association compliance. The law firm generates revenue — contingency fee settlements paid by insurance companies — and bears the direct costs of delivering legal services: attorney compensation, paralegal salaries, malpractice insurance, and case costs. Importantly, the law firm also pays the MSO a management fee for the services the MSO provides.

What moves to the MSO: Marketing and advertising, intake operations, HR, finance and accounting, IT and technology, office leases, call center operations, vendor relationships, and brand assets. The MSO generates revenue through the management fee it charges the law firm. It bears the costs of delivering all those operational services.

The critical compliance principle — which legal ethics counsel emphasize — is that the MSO's fee cannot be a percentage of legal revenue or contingency fees. That would constitute fee-sharing with a non-lawyer, which is prohibited in 48 states. The fee must reflect fair market value for the services the MSO actually provides.

The Two Compliant Fee Structures

There are two dominant payment models in legal MSO transactions, and understanding the difference shapes how investors value your MSO at the moment of a sale.

The flat-fee model sets a fixed monthly payment from the law firm to the MSO, regardless of firm performance. This is simpler and more predictable for both sides. The risk is that if the MSO drives case volume significantly higher, the law firm captures most of that upside — which investors may push back on through deal structuring.

The cost-plus model reimburses the MSO for its actual operating costs plus a fixed percentage margin, typically 10–20%. This is better aligned with the MSO's investment risk: if the MSO spends more on marketing and intake to grow the platform, it earns a proportional return on that spend. In a typical cost-plus arrangement, if the MSO invests $8M to scale marketing and drives firm revenue from $5M to $12M, the MSO earns its margin on that $8M — all without a single dollar of that income being tied to legal fee percentages.

A Worked Example: Before and After the Carve-Out

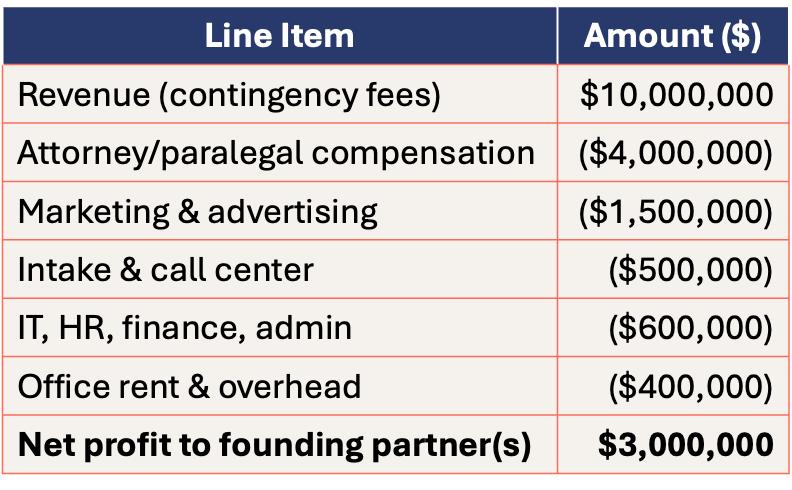

Let's make this concrete. Assume a PI firm generating $10M in revenue at a 30% margin — $3M in annual profit that flows entirely to the founding partner.

Before the MSO carve-out, the income statement looks like this:

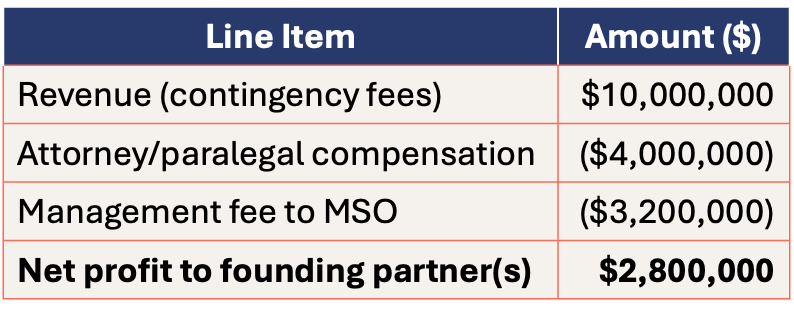

After the carve-out, the law firm's income statement simplifies dramatically. All the non-legal functions leave the firm's books. The law firm pays a single management fee to the MSO:

Law Firm (PC)

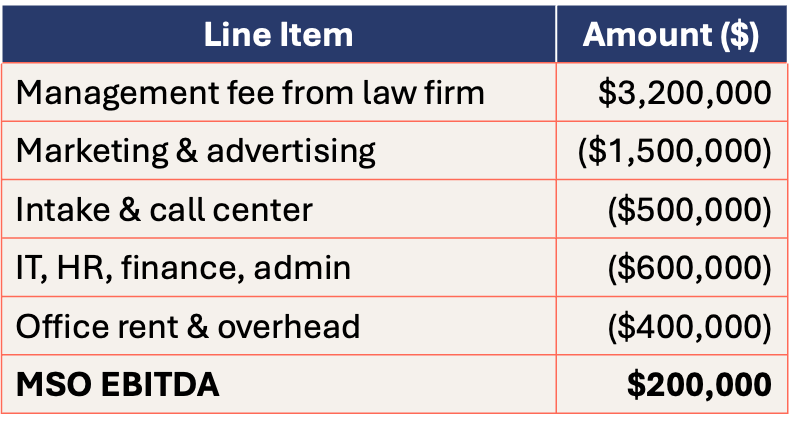

Management Services Organization (MSO)

At formation, the MSO earns a modest return — roughly 6% — reflecting fair market value for the services it provides. This is intentional and correct. The goal at this stage is structural compliance, not maximum MSO profitability.

How the MSO Gets Valuable

Here's the shift that makes investors pay attention. When an outside acquirer enters the picture — a PE firm executing an MSO roll-up strategy — they're not just buying the current economics. They're buying the ability to scale them.

The MSO model unlocks three levers that a traditional standalone firm cannot access:

Operational leverage through shared infrastructure. Once the MSO is managing intake, technology, and marketing for not one firm but five, the fixed cost base spreads across a larger revenue pool. Marketing campaigns that cost $1.5M for one firm might serve a five-firm platform for $4M — roughly half the per-firm rate of going it alone. That margin improvement accrues entirely at the MSO level.

Multiple expansion at exit. A solo PI firm typically sells at 3–5x EBITDA, if there's a buyer at all. A scaled, multi-firm MSO platform with $25M in EBITDA and diversified geographic revenue can command 7–10x. The exit multiple is where the real wealth creation happens.

Revenue growth from professional management. L.E.K. identifies personal injury as the highest-fit practice area for MSO value creation, precisely because marketing spend, case intake conversion, and operational efficiency are all measurable and improvable with institutional resources. A founding partner who was spending $1.5M on TV advertising with no attribution data suddenly has a CMO and a data team optimizing every dollar.

What This Means for You as the Seller

Return to our $10M firm. Assume an acquirer enters, implements a platform MSO across five comparable firms, and exits four years later. Your $3M-per-year law firm was valued at acquisition on the MSO's earnings potential — say $2M in year-one MSO EBITDA across the platform, priced at 6x for a total enterprise value in the low-to-mid eight figures.

You take the majority of your proceeds in cash at close. You roll a portion — typically 20–30% — back into equity in the combined platform. Over four years, the platform grows, margins improve, and the exit multiple expands. Your rolled equity, which represented a single firm's contribution at inception, is now part of something worth multiples of what you sold into.

The founding partner's total economic outcome isn't just the check at closing. It's the check, plus the second bite of the apple that the rollover equity generates when the platform sells. As we've written elsewhere on this site, a firm owner who enters a roll-up at a 4x entry and exits at an 8x multiple — with margin expansion along the way — can realistically see their rollover equity grow 3–4x. That's the compounding effect of platform economics that a standalone firm can never replicate on its own.

The Bottom Line

The MSO model doesn't just give you a mechanism to bring in capital. It restructures your business in a way that makes the non-legal half of your operation — the marketing, the intake engine, the back office — into a standalone, investable asset with its own income statement, its own investors, and its own valuation. That asset is where outside capital lives, where platform economics compound, and where the real exit premium gets created.

The question is not whether to understand this. The question is whether you're positioned to take advantage of it when the right counterparty arrives.

Stonecutter Group advises personal injury firm owners on capital strategy, MSO readiness, and investor partnerships. If you're evaluating your options, we'd like to hear from you.

Sources

L.E.K. Consulting. "How Investors Evaluate Legal MSO Opportunities." February 27, 2026. lek.com/insights/business-services/how-investors-evaluate-legal-mso-opportunities

Stonecutter Group. "The 7 Steps to Transform Your Law Firm Using an MSO Structure." March 10, 2026. stonecutter.group/insights

Stonecutter Group. "The Legal Industry Is About to Change." February 17, 2026. stonecutter.group/insights

Reed Smith LLP. "Private Equity and the Business of Law: Recent Market Trends in MSOs and Alternative Structures." February 5, 2026.